Chapter 19 – Foreign Direct Investment in the United States

I. Country Snapshot

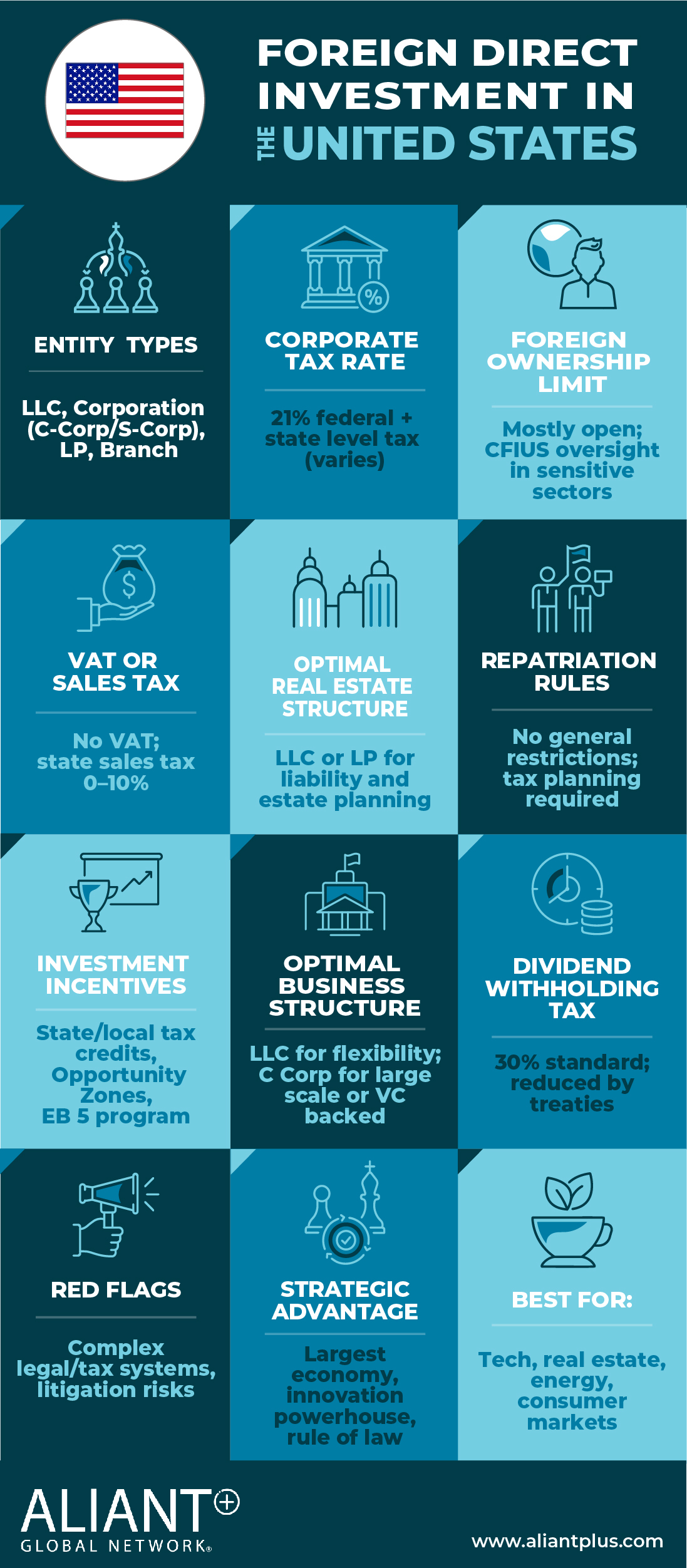

II. Introduction

Investing in the United States presents foreign investors with unique opportunities and challenges. The U.S. welcomes foreign investors and has minimal limitations on what types of assets can be purchased. The U.S. also has a transparent judicial system, very limited corruption, and no currency controls.

Critical considerations include selecting the right corporate structure, minimizing tax liability, and limiting exposure to legal risks (like lawsuits). The flexibility of U.S. business entities (corporations, limited liability companies and limited partnerships) makes them particularly attractive for various investment scenarios. The following provides an overview of key U.S. legal and tax issues affecting foreign investors and offers insights into optimal structures for both real estate and business investments.

III. Ownership Structures

Foreign investors can choose from several ownership structures when acquiring U.S. assets, including direct ownership, a limited liability company (LLC), a limited partnership (LP), a U.S. or foreign based corporation, or a combination of the above. Each structure offers distinct advantages based on the investor’s goals, such as liability protection, tax efficiency, and compliance with U.S. laws. Further, interests in legal entities may be owned by foreign investors directly or through a trust.

A. Direct Investment

Direct ownership is straightforward and involves a single level of tax on income and on asset sales. Long term capital gains are taxed at 15% or 20%. However, direct ownership lacks liability protection and privacy, and assets are subject to U.S. estate and gift taxes.

B. Flow – Through Entities – LLCs or LPs

LLCs and LPs offer significant flexibility in structuring ownership and operations, making them ideal for investment deals. They provide a single level of income tax, liability protection and allow for lifetime transfers without U.S. gift tax (and thereby also avoiding the estate tax). However, state filing requirements may reveal the names of managers or general partners, which can be addressed by utilizing Wyoming or Delaware LLC as the manager or general partner. The business activities of the LLC or LP in the United States will be attributed to the foreign investor, and the foreign investor may be required to file tax returns with the Internal Revenue Service.

C. U.S. Corporation

A U.S. corporation provides liability protection and privacy but involves double taxation of income: once at the corporate level and again on dividends paid to foreign investors. Shares in the corporation are also subject to U.S. estate taxes and attachment by judgment creditors. Ownership of corporate shares is deemed a purely passive activity, and the business of the corporation is not attributed to the foreign owner. This means that if a foreign investor owns U.S. real estate or a business through a U.S. corporation, the foreign investor will not have to file a U.S. tax return.

D. Non – U.S. Corporation

A non-U.S. corporation offers liability protection and avoids U.S. estate taxes on shares. However, it may face corporate level taxes and limited tax treaty benefits.

IV. Suggested Structures for Real Estate and Business Investments

Real Estate Investments

- Optimal Structure: A non S. corporation owning a U.S. LLC taxed as a corporation.

- Why: Provides liability protection, estate tax exclusion, and control over distributions while avoiding direct taxation of the non U.S. corporation.

- Bonus: A foreign investor should consider holding the shares of the non S. corporation in an offshore trust, for further tax minimization and liability protection.

Business Investments

- Optimal Structure: A S. LLC or LP for operational flexibility and tax efficiency.

- Why: Offers liability protection, flow through tax benefits, and adaptability for various business operations.

- Bonus: Consider ownership of the LLC through a U.S. corporation to preclude the requirement to file U.S. tax returns. Further consider holding corporate shares in a U.S. or foreign trust.

V. Simplified Tax Overview

U.S. tax laws for foreign investors depend on the structure chosen. Flow through entities like LLCs and LPs pass income directly to owners, avoiding corporate level taxes. Conversely, corporations face double taxation but provide privacy and liability protection and do not require investors to file U.S. tax returns. Proper planning can minimize estate and gift tax exposure, particularly when non U.S. corporations are used.

VI. Conclusion

Taken together, United States offers attractive openings for well‑structured investments when investors align with local compliance requirements and leverage available incentives. With prudent structuring, effective tax rates and regulatory friction can be kept competitive, allowing foreign entrants to capture long‑term growth.

Conclusion

The Right Structure, Place, and Time

Foreign direct investment is one of the most effective ways to scale wealth and business operations internationally. But it’s not just about entering new markets—it’s about entering them well. The difference between a profitable investment and a prolonged headache often lies in the early decisions: how the structure is set up, how the capital enters, how the profits are repatriated, and how the investor is protected.

This white paper is the product of decades of cross-border experience. From capital flows in China to real estate acquisitions in Spain, we’ve worked across sectors, continents, and legal systems to ensure that our clients enter new markets with confidence.

The lawyers and accountants of the Aliant+ Global Network don’t just interpret laws; we solve for business realities. Our approach is collaborative, pragmatic, and grounded in results. We’ve structured SPVs in Dubai, negotiated tax holidays in Hungary, navigated real estate traps in Italy, and built holding company frameworks that withstand scrutiny in both home and host countries.

If you’re reading this, chances are you’re considering an international investment, expansion, or strategic restructuring. When you’re ready to take that step, we’re here to guide you through it with the legal precision, international foresight, and practical clarity that global investment demands.